Mortgage Licensing School & Center For Mortgage Education | SAFE MLO Exam Prep

SAFE MLO Exam vs. OnCourse Learning

When preparing for the SAFE Mortgage Loan Originator (MLO) Exam, choosing the right exam preparation tool is critical to success. Two well-known platforms are OnCourse Learning by Colibri and SAFE MLO Exam. While both aim to help candidates succeed, SAFE MLO Exam offers unique advantages.

Home Mortgage Disclosure Act (HMDA) for the SAFE MLO Exam

If you’re preparing for the Mortgage Loan Originator (MLO) NMLS Licensing Exam, mastering key laws like the Home Mortgage Disclosure Act (HMDA) is essential. HMDA plays a vital role in mortgage lending compliance, fair lending practices, and preventing discrimination. Understand HMDA and pass.

SAFE MLO Exam vs. Mortgage Educators & Compliance (MEC)

When preparing for the SAFE MLO licensing exam, choosing the right test preparation package can make all the difference. This article compares two popular options: Mortgage Educators and Compliance (MEC) and SAFE MLO Exam. We’ll explore their features and benefits to help you make the right choice.

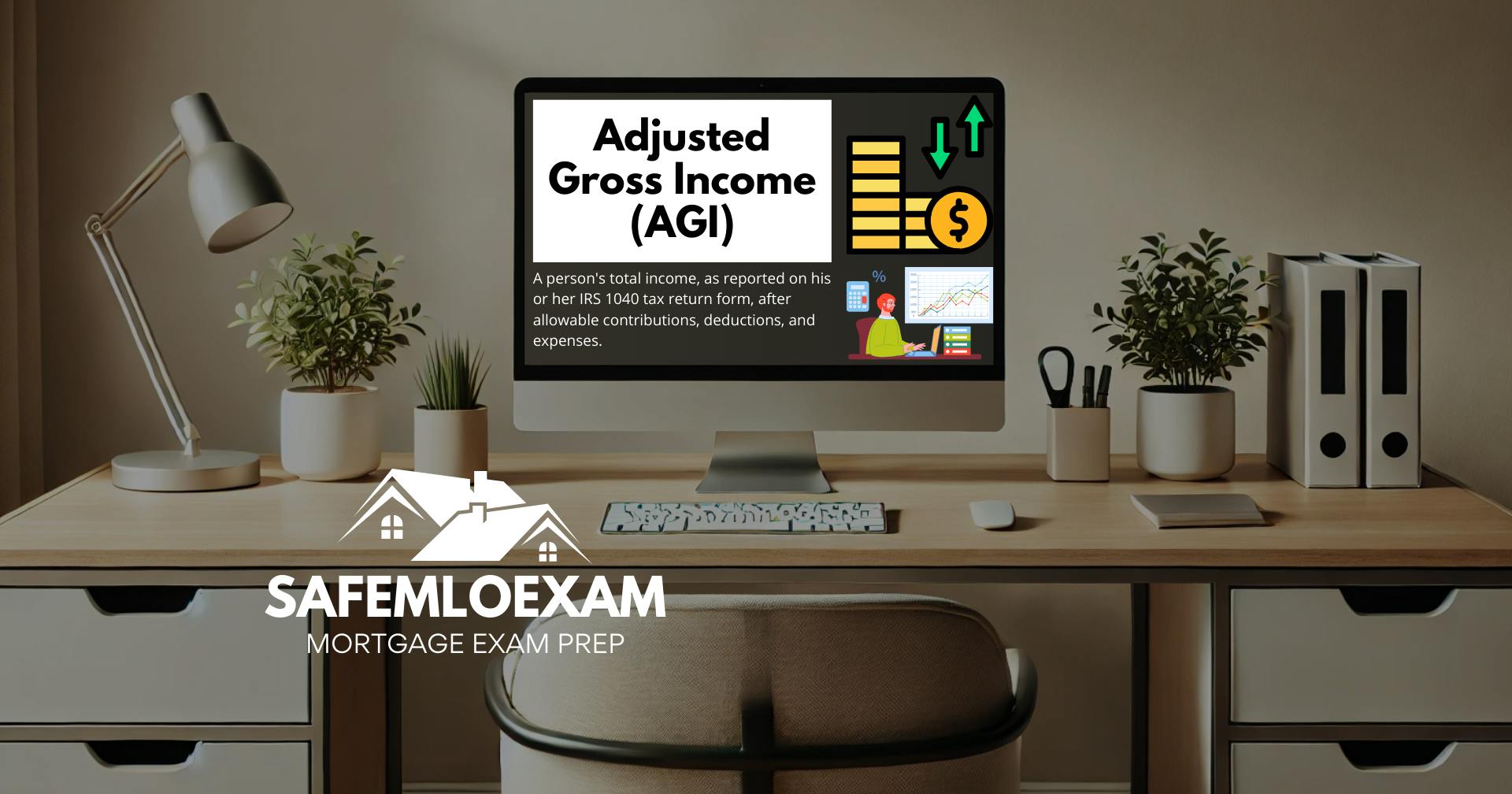

Adjusted Gross Income (AGI) for the SAFE MLO Exam

Are you preparing for the NMLS Mortgage Loan Originator (MLO) licensing exam? Understanding financial terms like Adjusted Gross Income (AGI) is essential for passing the test and excelling in your career as a mortgage professional. Let's break down AGI for mortgage calculations and loan underwriting.

Mortgage Loan Originator (MLO) Exam Prep

If you’re aiming to become a licensed mortgage loan originator, thorough preparation is non-negotiable. The NMLS SAFE MLO Exam is a challenging test designed to ensure only the most prepared candidates succeed. SAFE MLO Exam provides a complete Mortgage Loan Originator (MLO) Exam Prep solution.

SAFE MLO Test Prep: Your Key to Exam Success

Preparing for the NMLS SAFE Mortgage Loan Originator Exam can feel like an uphill battle, but the right resources make all the difference. SAFE MLO Exam offers an all-encompassing SAFE MLO Test Prep program designed to take the guesswork out of studying and help you achieve your goals efficiently.

Mortgage License Test Prep: A Guide to SAFE MLO Exam

Obtaining your mortgage loan originator license is a significant step in building a rewarding career in the mortgage industry. However, the journey begins with thorough preparation for the NMLS SAFE MLO Exam. SAFE MLO Exam offers a comprehensive Mortgage License Test Prep solution.

NMLS Practice Test Free: Get Started With My Mortgage Test

Preparing for the NMLS SAFE Mortgage Loan Originator (MLO) Exam can be overwhelming, especially if you’re just beginning your journey. One of the best ways to ease into your studies is by utilizing a free mortgage practice test. At SAFE MLO Exam, we understand how important it is to assess your exam readiness.

Free NMLS Practice Test Questions to Pass the Exam

Success on the NMLS SAFE MLO Exam starts with preparation, and the key to preparation lies in practice. SAFE MLO Exam offers an unparalleled collection of NMLS Practice Test Questions that help aspiring mortgage loan originators achieve their goals. Here’s why we're the gold standard for exam readiness.

Master the NMLS Exam with SAFE MLO Exam Prep

Preparing for the NMLS SAFE Mortgage Loan Originator (MLO) Exam can be a daunting task, but the right resources make all the difference. With SAFE MLO Exam Prep, you gain access to a robust suite of tools designed to simplify your journey to licensure and career success. Let’s explore SAFE MLO Exam.

SAFE MLO Exam Prep NMLS Practice Test Questions

If you’re preparing to take the NMLS SAFE Mortgage Loan Originator (MLO) Exam, having access to the best resources is crucial for success. SAFE MLO Exam provides an all-inclusive exam prep solution designed to make your preparation process efficient, effective, and comprehensive.

Top Strategies to Pass the NMLS SAFE MLO Exam

The NMLS Mortgage Loan Originator SAFE MLO Licensing Exam is a crucial milestone for aspiring mortgage professionals seeking to build a successful career. Passing this exam not only validates your knowledge of mortgage lending but also sets the foundation for your role in the industry.

NMLS Login Resource Center

Any successful MLO must be familiar with navigating the Nationwide Multistate Licensing System (NMLS). It is an absolute necessity for mortgage industry professionals, especially Mortgage Loan Originators (MLOs). The NMLS is the main registry for MLOs. It makes obtaining and renewing your MLO license simple. It also lets you track your continuing education (CE) requirements to ensure that you meet the requirements and allows you to manage your licensing requirements across every state.

WHAT DOES IT TAKE TO PASS THE NMLS EXAM?

What Does it Take to Pass the NMLS Exam? Advice from an Experienced Exam Prep Trainer By SAFE MLO EXAM PREP & Rich Leffler Let’s face it! There are many more appealing activities in which one can get busy than preparing for an exam, especially the NMLS National MLO Licensing Exam. But plainly and simply, if...

NMLS TEST PREP – 1,000 NMLS PRACTICE TEST QUESTIONS

NMLS Test Prep – 1,000 NMLS Practice Test Questions Once SAFE MLO Exam Prep has thoroughly prepared you to successfully tackle the NMLS licensing exam, it’s time to schedule your exam. To do so, the test candidate should visit the NMLS’ Testing page

HOW TO BECOME A LOAN OFFICER

How To Become A Loan Officer – The Licensing Process Applying for a mortgage loan originator’s license involves a process that includes: Registering through the NMLS’ website and securing one’s NMLS unique identifier Completing the 20-hour preliminary licensing education course Taking advantage of additional but optional mortgage exam preparation through a quality NMLS national test […]

NMLS – NATIONWIDE MULTISTATE LICENSING SYSTEM & REGISTRY

What Is The NMLS – Nationwide Multistate Licensing System & Registry NMLS History & Background I remember landing my first mortgage job as a Mortgage Customer Service Representative for a large bank in Buffalo, New York. The year was 1996 and, even though I had no previous mortgage or banking experience, the bank liked me […]

MINNESOTA AND WEST VIRGINIA STATE TEST COMPONENTS OF THE SAFE MLO TEST WILL NO LONGER BE OFFERED OR ADMINISTERED BY NMLS

Minnesota and West Virginia State Test Components of the SAFE MLO Test will no longer be offered or administered by NMLS It was recently announced by NMLS that, effective September 1, 2018, the “Minnesota and West Virginia State Test Components of the SAFE MLO Test will no longer be offered or administered by NMLS. Candidates […]

FHFA Increased Annual Loan Limit VA Loans 2018

FHFA Increased Annual Loan Limit VA Loans 2018 FHFA Increased Annual Loan Limit VA Loans – SAFE MLO EXAM is pleased to report that for 2018, The Federal Housing Finance Agency (FHFA) has increased the annual loan limits beyond which jumbo financing would be required, which includes VA loans. The 2017 conventional/conforming loan limit for […]

California Mortgage Exam Prep

California Mortgage Exam Prep Every mortgage professional who originates loans in the state of California must be licensed. And being licensed means having to pass the National Mortgage Licensing System (NMLS) pre-licensing exam. The exam is relatively standard. SAFEMLOExam.com is a California mortgage exam prep solution that helps test takers pass their exam. It includes […]

The Different Mortgage Career Paths In California

The Different Mortgage Career Paths In California There are hundreds of career options in the mortgage industry and for those interested in starting a mortgage career in California, taking a mortgage exam is compulsory and this is why it is advisable that you take a mortgage preparatory exam like NMLS Practice Tests to hone your […]

YOUR LICENSE IS YOUR BUSINESS – MORTGAGE LICENSE RENEWAL

Your License is Your Business Campaign: SRR and NMLS’ Ticket in Educating and Informing Everyone about Mortgage License Renewal Whenever business owners would like to establish their own business venture, the first thing that they prioritize is their mortgage license because it certifies that their business is legal and is authorized to operate. Many businesses […]

Changes That You Need to Know About Renewing Your Mortgage License

Changes That You Need to Know About Renewing Your Mortgage License So, you need to renew your mortgage license that you obtained after much hard work and taking practice test after practice test? Do you already know about the latest changes in the renewal process? If you don’t, then you better read this article for […]

Mortgage Training Expansion in California

SAFE MLO Exam Discusses Mortgage Training Expansion in California The mortgage industry has experienced slow growth, even though there is a strong demand for housing in recent years. Hence, an expansion in reverse mortgages is required to provide a boost to further strengthen the industry. The largest California mortgage broker has taken a new approach […]

Real Estate Agent vs. Mortgage Broker – Which One Is Better?

Real Estate Agent vs. Mortgage Broker – Which One Is Better? So, you do have plans to start a career in the real estate industry? If you are, then for sure, you are quite confused on as to whether you should just take the NMLS SAFE MLO national mortgage loan originator exam and become a […]

Pass the NMLS SAFE MLO Exam the First Time

Pass the NMLS SAFE MLO Exam the First Time Your dream may to become a licensed NMLS SAFE MLO mortgage loan originator. Why not? Being an MLO will open your door to different career opportunities. The majority of the mortgage companies provide substantial perks and benefits, including sales commission, bonus pay, health insurance, advertising and […]

HOW TO GET AN NMLS SAFE MORTGAGE LOAN ORIGINATOR (MLO) LICENSE

Licensing Requirements for Mortgage Loan Originators: How to Get an NMLS SAFE Mortgage Loan Originator (MLO) License As a mortgage loan originator, you usually have two jobs; one is to persuade people that their lending reputation is the perfect borrowing option and the second is to assist people in navigating the closing table. At first, […]

NEW YORK OFFICIALS EXPANSION OF NMLS TO IMPROVE ITS AUTHORITY

SAFEMLOExam.com on New York Officials Expansion of NMLS to Improve Its Authority New York’s Department of Financial Services made changes in the Nationwide Multistate Licensing System and Registry, NMLS, NMLSR. The transition aims to manage the license application process as well as the ongoing guidelines of the non-depository financial establishments who operate business in the...

LICENSE APPLICATIONS AND RENEWALS IN MARYLAND MIGRATING TO NMLS

SAFEMLOExam.com Examines License Applications and Renewals in Maryland Migrating To NMLS License applications and renewals in Maryland are migrating to NMLS upon the enactment of House Bill 182. Said bill requires debt collectors and licensees to migrate their license applications and renewals to NMLS (a/k/a Nationwide Multistate Licensing System and Registry). This only means that...

HOW TO BECOME A PROFESSIONAL MORTGAGE LOAN ORIGINATOR

SAFEMLOExam.com on How to Become a Professional Mortgage Loan Originator (MLO) In this very competitive world, only the most dedicated and persevering people remains on top and become a professional Mortgage Loan Originator. It is therefore highly suggested for you to make great efforts to be the best in your specific niche. Among the most...

SAFEMLOExam.com Shows You How to Become a Licensed Mortgage Loan Originator (MLO)

SAFEMLOExam.com Shows You How to Become a Licensed Mortgage Loan Originator (MLO) Mortgage Loan Originator (MLO) is a popular financial career, where smart and capable people willing to do what it takes will have the opportunity to succeed. If you have the willingness to study, work hard and be a professional with integrity, a career...

FAQ’S ABOUT THE NMLS EXAM

SAFEMLOEXAM.COM’S FAQ’s about the NMLS Exam – SAFE MLO (Mortgage Loan Originator) Test Are practice tests important while studying to take the NMLS Exam? Yes. Taking as many practice tests as you can, such as those available on SAFEMLOExam.com, will greatly assist you in preparing for the SAFE MLO exam. Where can I get accurate...

Become a Mortgage Broker – First Pass Your Mortgage Test with SAFEMLOExam.com

Become a Mortgage Broker – First Pass Your Mortgage Test with SAFEMLOExam.com Learn all about how to become a successful Mortgage Broker. Have fun at your work, feel fulfilled, and help others fulfill a lifelong dream! Owning a home remains on the wish lists of millions of hard-working and stable Americans. Thus, there is always...

SAFEMLOExam.com Provides Comprehensive Tips for Passing the SAFE MLO Exam

SAFEMLOExam.com Provides Comprehensive Tips for Passing the SAFE MLO Exam Feeling nervous about your upcoming SAFE MLO exam? In order to become a professional, trusted and licensed mortgage loan originator, you have to pass the SAFE MLO exam. In fact, it will be better for you to pass it on the first try so you...

SAFEMLOEXAM.COM SHOWS YOU HOW TO GET A MORTGAGE BROKER’S LICENSE THE EASY WAY

SAFEMLOExam.com Shows You How to Get a Mortgage Broker’s License the Easy Way! Users of safemloexam.com, the best site for online practice SAFE MLO exams, are asking if there is an easy way to get a Mortgage Broker’s License. If you have any plans to start a career as a mortgage broker, then the very...

The Purpose of SAFE Legislation

The Purpose of SAFE Legislation The SAFE Legislation or the Secure and Fair Enforcement for Mortgage Licensing Act of 2008 was passed on July 30, 2008. This federal legislation provided a time allotment of one year for each individual state to pass their own legislation to ensure the licensure of mortgage loan originators meet national...

SAFE MLO Exam 101 – Introduction, Origin, Structure & Fees

SAFE MLO Exam 101 – Introduction, Origin, Structure & Fees Introduction The SAFE MLO Exam or SAFE Mortgage Loan Originator Exam is a required exam in all US jurisdictions and States to comply with the SAFE Act.